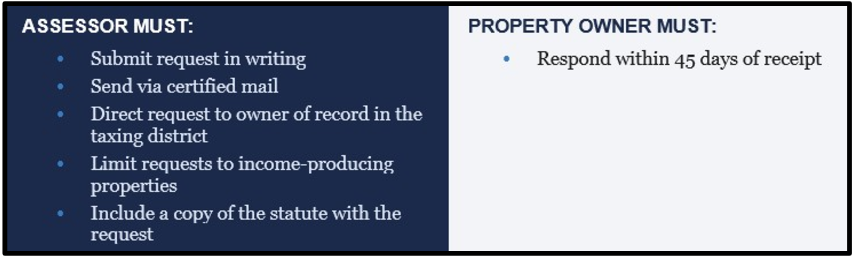

Pursuant to N.J.S.A. 54:4-34 (“Chapter 91 Statute”), New Jersey municipalities are authorized to send “Chapter 91” requests to owners of income- producing property requesting income and expense details. These requests are issued by each municipality’s tax assessor who uses the information collected to set property tax assessments for the following year. The purpose in obtaining the requested information is to enable tax assessors to correctly assess income-producing properties and thereby avoid unnecessary expense, time and effort in tax appeal litigation.

Download Printable Article (PDF) >>>

The 45-Day Deadline for Chapter 91 Requests

If a property owner fails to respond to an assessor’s request within forty-five (45) days, the property owner is prevented from appealing their assessment. It is essential that property owners react accordingly when presented with the assessor’s request. However, the assessor’s request must comply with the Chapter 91 Statute.

Chapter 91 Statutory Requirements at a Glance

Consequences of Non-Compliance and Good Cause Exception

If the property owner fails to respond within forty-five (45) day period, the assessor must value the property based upon all available information and attempt to determine the full and fair market value of the property. This often results in a much higher assessment, and therefore taxes, that the property owner would prefer.

The penalty imposed on property owners for failing to respond is a loss of its right to appeal the assessor’s assessment. However, Chapter 91 statute creates a “good cause” exception for the County Boards and courts to consider when the property owner cannot furnish the information within the required period.

Although straight forward, Chapter 91 disputes constitute a surprising amount of litigation in the Tax Court. Every year there are disputes as to whether (i) the request was received, (ii) whether the assessor complied with the statute, (iii) whether a sufficient response was provided by the property owner, and (iv) whether the good cause has been shown to allow the appeal to continue.

Why Chapter 91 Requests Matter in Real Estate Transactions

Complying with your Chapter 91 Request not only benefits property owners in avoiding litigation, but also in the eventual sale of their property. Purchasers of commercial property are cognizant of the taxes due on the property. Savy buyers often request evidence that the Seller has complied with its Chapter 91 Request to ensure an appeal of the property’s taxes can be made. This is very important where the purchase price is less than the property’s equalized value.

With the 2026 tax appeal deadline now passed, property owners and real estate professionals should be on the lookout for the next wave of Chapter 91 requests. These requests are typically mailed out by the assessor anytime between May and November.

About Kulzer & DiPadova, P.A

Kulzer & DiPadova, P.A. is a law firm with more than 50 years of experience guiding individuals and businesses through complex estate, tax, and business matters. What sets our firm apart is depth of expertise: every attorney holds a Master of Laws (LL.M.) in Taxation, and several are also Certified Public Accountants (CPAs). We proudly serve individuals and businesses across New Jersey and the Greater Philadelphia area.

FOR MORE INFORMATION CONTACT:

William H. Dungey III, Esquire

Kulzer & DiPadova, P.A.

76 E. Euclid Avenue, Suite 300

Haddonfield, NJ 08033

(p) 856.887.4717

www.kulzerdipadova.com

WDungey@kulzerdipadova.com